Table of Contents

India is a mesmerizing country that stretches across the heart of South Asia, encompassing a tapestry of diverse cultures, breathtaking landscapes, and a rich historical heritage. Nestled between the towering Himalayas to the north and the azure waters of the Indian Ocean to the south, India is a kaleidoscope of experiences that beckons travellers, explorers, and digital nomads worldwide.

India’s cultural heritage is a captivating mosaic woven together by centuries of history. From the regal palaces of Rajasthan to the intricately carved temples of Tamil Nadu, every corner of India resonates with its own unique story. Festivals like Diwali, Holi, and Eid transform the country into a riot of colours and celebrations, offering visitors a firsthand glimpse into its vibrant traditions and close-knit communities.

The geography of India is as diverse as its people. The tranquil backwaters of Kerala, the lush tea gardens of Darjeeling, the golden deserts of Rajasthan, and the pristine beaches of Goa—all come together to create a visual symphony. The towering peaks of the Himalayas offer breathtaking trekking routes and spiritual retreats, while the vast Thar Desert promises unforgettable camel safaris beneath star-studded skies.

Indian cuisine is a culinary adventure that dances on the taste buds. From the fiery curries of the south to the aromatic biryanis of the north, each region boasts its own mouthwatering specialities. Street food stalls offer an array of chaats, kebabs, dosas and sweets that are a delightful indulgence for your senses. Exploring India’s food scene is like embarking on a gastronomic journey that unveils the country’s soul.

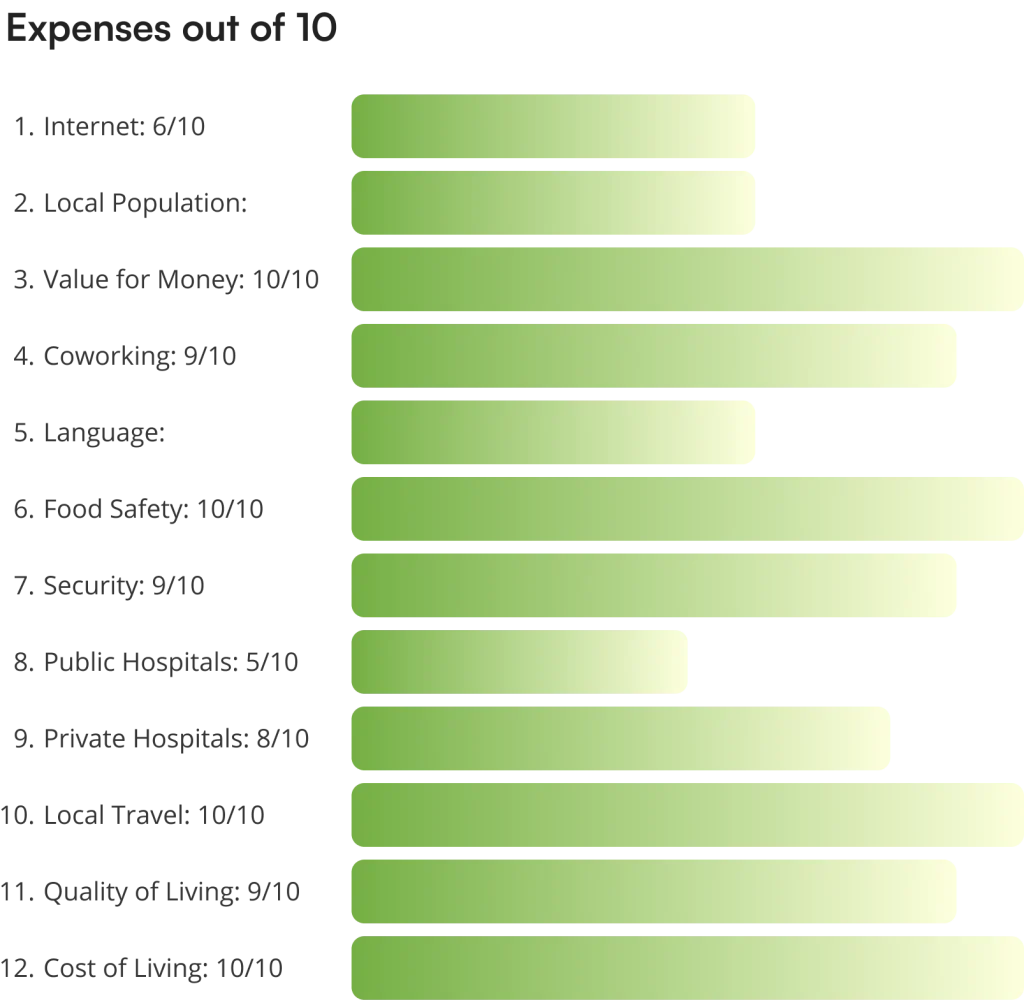

India’s blend of old-world charm and modern connectivity makes it an enticing destination for digital nomads. Bustling cities like Bangalore and Mumbai offer a dynamic environment for networking, while serene retreats in the Himalayas or the coastal towns provide the tranquillity necessary for productive work. High-speed internet and co-working spaces have sprouted across the country, fostering a community of freelancers, entrepreneurs, and remote workers.

140.76 crores (as of 2021)

Indian Rupee (₹)

In northern areas like Delhi, Agra, and Rajasthan, temperatures can drop to around 5°C (41°F) or lower. The states lining the Himalayas often experience snowfall and negative temperatures, while most coastal states boast a steady 20-35°C (77°F to 95°F).

Pack: Warm layers, sweaters, and jackets for north India & lighter clothing for south India.

Food Delivery Apps in India

> Zomato

Zomato delivers food from restaurants and also offers dining recommendations along with discounts.Swiggy

Swiggy offers food delivery from restaurants and other essentials through its sub-platform – InstaMart (available on the same app)

Get it here:

iOS | AndroidApps to Rent Cabs in India

The best apps to rent cabs in India are Ola, Uber and BluSmart.

You can also book tuktuks and motorcyle taxis in India on Rapido, apart from Ola and Uber.

Apps to Order Groceries in India

The best apps to order groceries in India are Blinkit (delivery in under 15 minutes), InstaMart (on the Swiggy App) and Dunzo (can also do personal deliveries within 10kms).

PS: Currently, Zomato, Swiggy and InstaMart are the only functional apps in smaller towns and states like Goa.

Dating Apps in India

NomadGao recommends Bumble and Aisle for an optimum dating experience in India. If you are open to experimenting, try out the more digital nomad friendly-apps such as Fairytrail and Nomad Soulmates.

Travel Booking Apps in India

> Use SkyScanner if you want to book flights in India.

Use IRCTC if you want to book trains in India (you will have to sign up and pay a small fee to register as an international tourist.)

Pro tip: Your international Credit Card may not work on IRCTC website. We recommend that you use AMEX if possible or book through an agent for a smoother process.Use Make My Trip if you want to book buses in India.

Shopping Apps in India

> Myntra, for shopping clothes, makeup and accessories.

> Amazon, for all essentials.

Network Provider Apps in India

The best network provider to use in India is Jio or Airtel. You can know more about getting a SIM in India, here.

Hotel Booking Apps in India

The best apps to book a stay as a digital nomad in India are Airbnb, Hostel World and Booking.com.

Medical Apps in India

If you want to get medicines delivered in India, use:

> Wellness Forever

> Apollo- Other Apps in India

> If you are looking for events in India, try Book My Show or Paytm InsiderCultFit gives access to home workout, gym or other fitness memberships in India.

UPI is one of the many services that revolutionised digital payments in India. Anyone with a bank account can now transfer funds with a single tap.GPay PhonePe and Paytm work well in India but may not have the same user case worldwide i.e. one country’s application does not work in other countries.If you are an international digital nomad looking to simplifypayments in India through UPI, you can get a special wallet at select airports in India (Delhi, Bengaluru and Mumbai).As of now, the service is available primarily to residents of the G20 countries (Argentina, Australia, Brazil, Canada, China, France, Germany, India, Indonesia, Italy, Japan, Republic of Korea, Mexico, Russia, Saudi Arabia, South Africa, Turkey, United Kingdom and the United States), and the European Union.This can ease your struggles with credit cards and reduce your need for carrying liquid cash since a large business population in India may not accept cards.

Digital nomads in India enjoy travelling across the country – from the north to the south. Often they land in Delhi and head to the Himalayas from there – trekking, camping, working and enjoying warm mountain food. They then head down to Rajasthan to experience the land of the kings. If you want, you can also check out the northeastern states, but the infrastructure might not meet your remote work demands. From the mountains, you head down to the forests of the Western Ghats, the Konkan Coast, the southern-most tip of India and so on. There is plenty to do and experience in the country and all the time in the world may not be enough.

India’s rising urban centres are home to a wide range of coliving spaces that cater to the needs of both Indian and International residents.

The Void features cosy rooms and private bathrooms, as well as relaxing communal areas to meet fellow travellers and remote workers.

1. Accommodation:

2. Workspace: Approx INR 500-2500 OR 6-45USD/day

Here are the most recommended ones.

3. Food:

4. Travel:

5. Leisure: Cruises, Camping, Tribal visits, Igloo stays, Safaris, Cooking experiences, heritage tours, food tours,

6. Local Experiences: INR 1500-10000 OR 18-120 USD

Currently, Viator is the most reliable platform to book a local experience in India.

7. Health & Fitness: INR 1000-15,000 or 12 – 170 USD

These are some of the top private hospitals in India:

The complete details of each places

Let us know if you’re interestd in starting a NomadGao project in your home town

Subscribe to our newsletter and be the first to know about exclusive promotions, travel inspiration, news, and updates.